Local governments, being closest to citizens, provide essential public services and directly impact the lives of many people. Citizens’ interactions with local governments also have the potential of influencing how they view democratic institutions more generally. Analyzing local government spending data can be a means of assessing the quality of democracy by showing how resources are allocated, indicating responsiveness to constituents, policy priorities, disparities in resource allocation, governmental efficiency, favoritism and even corruption. However, delving into the world of government finances may seem daunting due to confusing terminology, intricate administrative processes, and inconsistencies in how official information is recorded and displayed. If you haven’t done so yet, check out our inaugural blog post of this Local Spending Series. It’s about the opportunities and challenges of using local government financial information. There we have briefly illustrated some of these issues using examples from Brazilian and South African municipalities.

In this second Local Spending Series post we aim to communicate what we believe to be basic information for effectively using this type of financial data. Consider it a simple map to walk through (a part of) the maze of public finances. In our previous post we have touched upon distinctions between budgetary and non-budgetary spending information; mentioned different stages of the budget cycle and how it refers to different budget documents; identified that some financial documents display committed values whereas others display verified values. Today we want to provide a basic outline to help people make more sense of some of these documents and terms.

More specifically, in this blog post we present a comprehensive overview of three processes generating local government financial information about spending: budgeting, public procurement, and singular disbursements. We will outline the rationale behind each process, mentioning key stages and requirements that constitute them, while also attempting to draw attention to the fact that, although these are different processes, they are nevertheless interconnected. When appropriate we also suggest how different stages in these processes can serve as sources of information for those interested in knowing more about how local governments allocate resources.

An overview of budgeting, public procurement, and singular disbursements

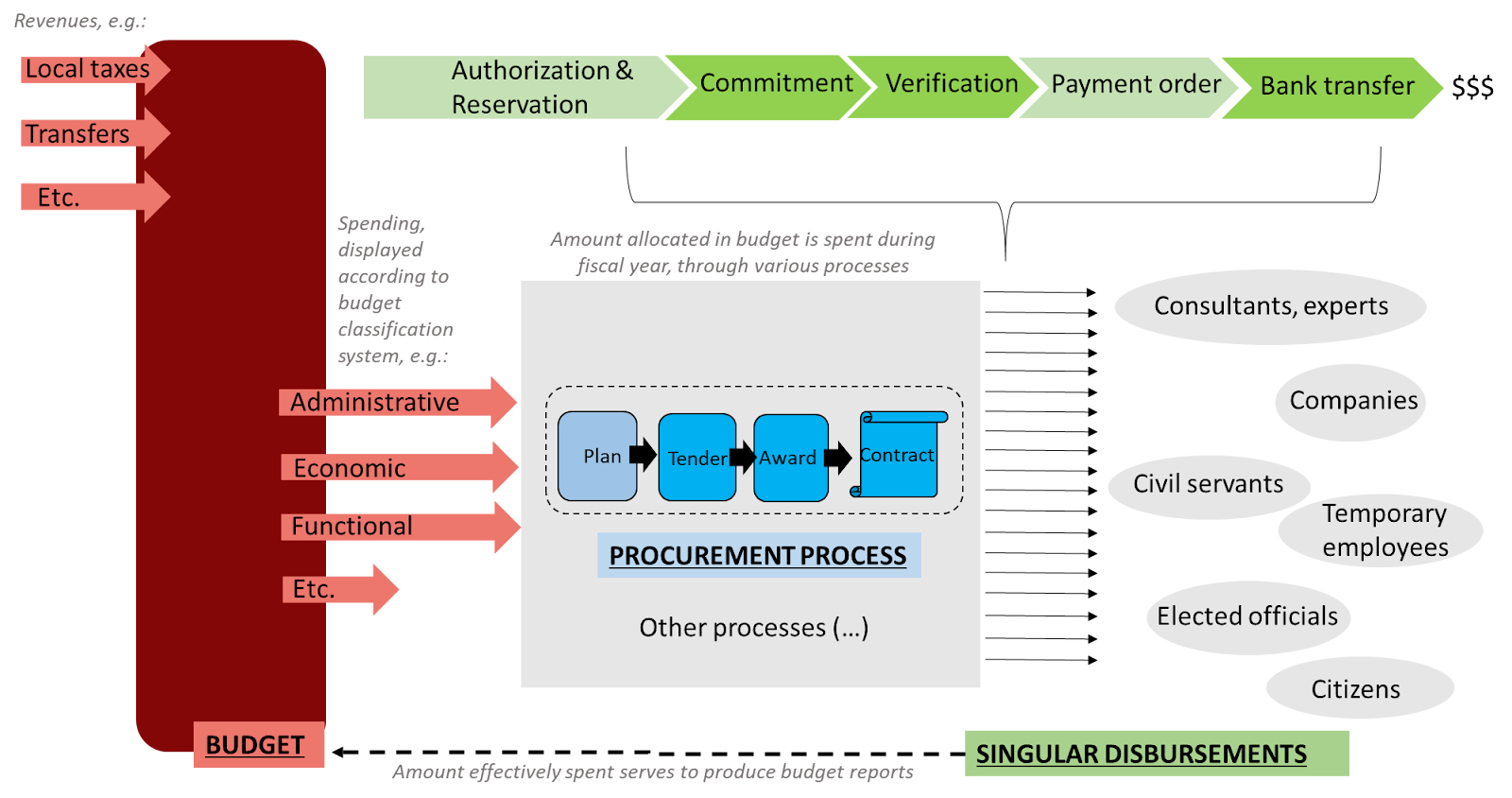

We start by providing a simplified illustration of the three processes and how they relate to each other in Figure 2:

In Figure 2, the burgundy box on the left side of the figure above represents the budget, more specifically the enacted budget, the document listing, amongst other things, all the spending in a given fiscal year. The arrows going into the box represent different sources of revenue whereas the arrows going out of the box represent spending. The spending information disclosed by documents depends on the classification systems employed by different budgeting practices, a topic we develop next.

The second process illustrated in the figure is the procurement process, represented by the blue boxes. Each blue box encompasses a different stage of procurement. We will explain later when a procurement process is usually necessary for the government to purchase goods and services, but in the figure above we already signal to the fact that not all individual transactions take place within a public procurement.

The third process represented in the figure is spending via singular disbursements. We represent the spending chain with green polygons. We also show that spending is grounded in the budget, and that there are many possible beneficiaries of such disbursements – that is, individuals or companies that directly receive monetary values from local governments, represented by gray ellipses – such as ordinary citizens, civil servants, and construction firms -. The multiple black arrows pointing to these beneficiaries show that some of that spending is encompassed in procurement processes – they refer to the implementation of contracts signed in the realm of procurement processes – whereas others do not. We return to these differences later. Lastly, we show a dotted arrow going from the green title “singular disbursements” to “budget”. We do that to represent the cyclical nature of budget, and the fact that different budget documents may report spending at different stages. We now refer to each of these processes individually. We start by focusing on the budget.

Budget

Budgeting constitutes a cyclical process, by which governments plan, discuss, decide, implement, and review the allocation of public resources. The budget is not just an outline of government spending, it also involves forecasting government revenues and justifying how the government intends to address its policy priorities and fulfill its fiscal responsibilities. While the fundamental concept of budgeting is perhaps universal, certain facets of this process vary across countries. For instance, some countries may incorporate a robust participatory element, enabling citizens to formally express their demands, whereas others may prioritize more rigorous audit procedures. There are, however, common stages in the budget cycle across different countries. A potentially useful resource to know more about the budget cycle in comparative perspective is the framework employed by the International Budget Partnership. Here we restrict ourselves to a more simplified version of this process.

A key aspect to have in mind when analyzing budget documents is the stage of the budget cycle when the document is produced:

- Typically, budget documents from the earlier phases tend to encompass more information about planned expenditures and conjectures, such as the Executive’s Budget Proposal, an annual policy document that translates key policy goals into budgetary plans.

- Once the legislative body approves the executive proposal, it becomes the Enacted Budget, serving as the foundational information for budget analysis during the fiscal year. This document will serve as a framework for the government, through its various departments and agencies, to go about their activities. These departments and agencies will pay their staff, or will hire companies to purchase goods to achieve policy goals. Through these administrative processes the resources which were once only formally destined to particular goals will be processed – and disbursed, as illustrated in Figure 2 – from the local governments to other beneficiaries.

- The information about singular disbursements is typically aggregated and fed back into the implementation and monitoring phase. In this feedback process periodic reports are issued to provide insights into budget impacts. The Year-End Report tends to be the most comprehensive. In simple terms, reports establish to what extent the formal allocation of resources was implemented, represented in Figure 2 by the arrow connecting “Spending” to “Budget”.

- Then the budget implementation can be audited, is to say impartially assessed by a different entity than the one spending and reporting government resources.

- Other than the documents produced at different stages of the budget cycle, different reports may have versions tailored for citizens comprehension, called Citizens’ Budget.

Crucially, the concreteness of expenditure information can vary depending on the stage of the cycle when the document is produced. Earlier documents will refer to values that are expected to be allocated but not yet spent, whereas later documents can serve to contrast expectations – that is, spending that was planned – to values that actually left local coffers. Some budget documents may also have different parts, some ‘forward looking’, listing resources which are planned to be spent, and others ‘past looking’, listing values that were actually disbursed.

Apart from the issue of concreteness of spending, another important aspect influencing the type of information disclosed in different documents concerns budget classification systems. International standards recommend that expenditures are broken down at least in terms of three types of classification:

- Administrative: concerns the department responsible for managing the funds, such as the education or health department.

- Economic: identifies the type of expenditure, commonly divided into operating expenditures, that is, expenses associated with routine operation, such as salaries or social assistance benefits, or capital expenditures, that is investments in long-term assets, such as infrastructure investments.

- Functional: encompasses expenditures according to the policy goals they are intended to address, as these may involve different departments, for instance, promoting access to affordable housing may involve the infrastructure and social assistance department.

Additionally, other classification schemes may be implemented. For idiosyncratic reasons different budget documents may employ different classification schemes, with different levels of detail. For instance, in some budget reports Brazilian municipalities expenses are classified also in programmatic terms, that is, in terms of how particular functional goals will be pursued, by specifying a policy program or policy action. In South African municipalities, the supporting documents of enacted budgets display capital expenditures according to, amongst other things, geographical classifications, indicating in which wards of a particular territory the money was spent, as shown in our previous blog post.

Consistent and detailed classification systems contribute to financial transparency, but the budget is ultimately a wide-encompassing process of government financial activity. Therefore, the insights in terms of spending practices that can be supported by budget documents are bounded by the classification system they adopt. Typically, to obtain more flexible, fine-grained information on expenditures, such as that identifying individual projects and beneficiaries, it is often necessary to resort to non-budgetary financial data, such as that generated by public procurement and singular disbursements.

Non-budgetary financial data: public procurement and singular disbursements

Public procurement and singular disbursements may also provide information about government spending, but as we have already mentioned when discussing Figure 2, the information differs, particularly in terms of detail and coverage.

All resources transferred from the local government to various beneficiaries, through its various departments and agencies, involve singular disbursements. At its earliest stage these resources can typically only be spent if they are accounted for in the budget. However, how these formal allocations actually lead to a transfer of resources may vary. Perhaps an enacted budget allocates 18 percent of resources to education, some of it to pay teachers, some to buy books, some to buy food to cook lunch for students, some to build new schools. How the 18 percent allocated to education will actually be spent will thus involve very different procedures: paying public employees tends to be subjected to a different set of regulations than hiring companies to build schools.

And why do governments need public procurement processes? Some types of governmental activities are executed directly by government staff. For instance, a local government department may have as employees street maintenance workers whose tasks involve sweeping streets, picking up litter, and removing debris. Other governmental activities may be too technical or demanding to be executed by government staff, and thus require hiring specialized companies. In these situations, governments often need to implement a public procurement process to select the most appropriate company to supply a given good or service for the best price. Because public procurement refers to an open competition, governments often are required to publish tender notices describing a particular need so that different companies can submit proposals. The award rules may vary with different types of procurement processes, but overall the award is a phase where the proposals are compared and the best one is selected. When the best proposal is selected the tender winner will sign the contract with the public entity, establishing the rights and obligations of both parties. As the contract is implemented the service and goods which were hired will be provided and the public entity will eventually pay for them.

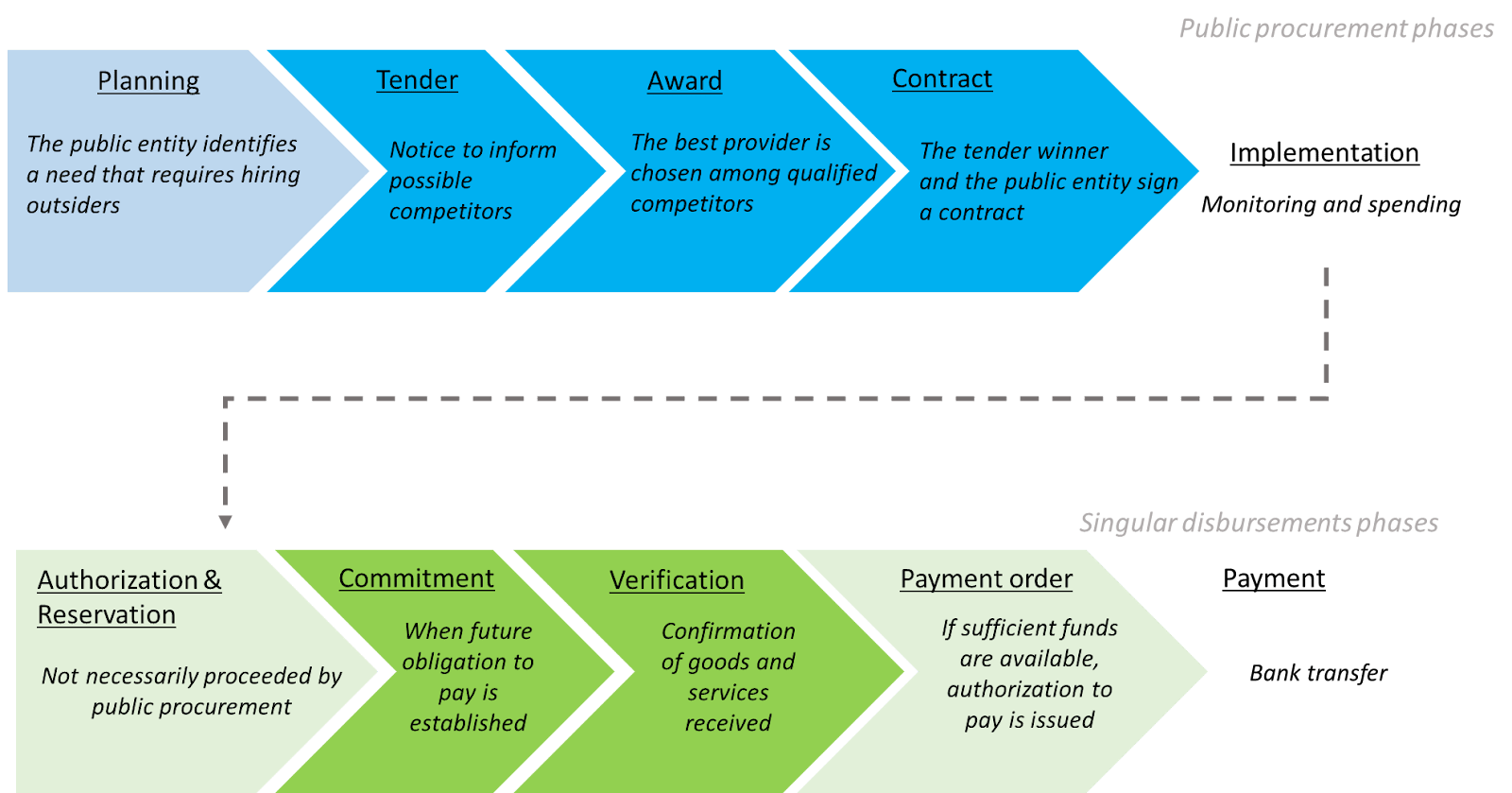

Inspired by the frameworks employed by the Open Contracting Partnership and by the IMF, in Figure 3 we zoom into the two processes, breaking them up into phases and briefly mentioning what these different phases encompass. We display some phases which we believe can be particularly valuable for data collection in more vibrant colors, and we discuss them in more detail below:

The blue polygons in the upper part of Figure 3 represent the public procurement process. Within this process, the tender and award stages involve publicizing a call for an open competition, establishing criteria for selecting the best vendor or service provider, and examining documents (or patterns) from these stages. Analyzing these stages can help assess if the company selection criteria were unbiased. This focus proves fruitful in investigating potential connections between those selected and individuals in positions of power, thereby determining the fairness of the procurement process. This analysis is particularly relevant in studies addressing conflicts of interest, favoritism, or cronyism.

Moreover, contracts, as significant documents within this context, offer valuable insights into government spending. Beyond detailing information about hired companies or individuals and outlining the responsibilities of all parties involved, contracts also provide information about specific projects. This information may include the project’s scope, allocated budget, technical specifications, and timeline. For that reason, analyzing contracts can offer a deeper understanding of government expenditures and shed light on the transparency and integrity of the procurement process.

The green polygons in the lower part of Figure 3 represent individual transactions. Despite the diverse purposes of different disbursements, they tend to share a common sequence of stages. Firstly, the disbursements must reference an amount allocated in the budget, and the relevant sectors within municipal administration must ensure the reservation of specific resources for expenditure. Secondly, a designated amount of resources must be committed to a particular function, establishing the government’s responsibility to make payments to external parties. Thirdly, authorities in charge must verify the actual supply or provision of goods and services. Fourthly, upon confirming the availability of sufficient funds, responsible authorities will issue an authorization to proceed with payment. Finally, the funds are disbursed from public coffers, completing the transaction process

Understanding various stages preceding disbursement matters, as values reported at different spending stages or processes serve distinct purposes. For example, an enacted budget—approved by the legislative body at the fiscal year’s outset—typically reflects spending in the form of committed values. However, budget reports may also present spending in the form of verified values or values that have been actually paid.

Researchers pursuing different objectives may focus on specific stages. Some researchers might be interested in the formal commitments governments make to particular goals, leading them to collect data on values committed to specific policy areas. On the other hand, researchers with a focus on assessing government effectiveness may prioritize information about values that have been actually spent. Thus, an awareness of the nuances in reporting at different spending stages is essential for researchers to gather data aligning with their research goals accurately.

Next steps

In this post, we’ve provided an overview of how budgeting, public procurement, and singular disbursements within local governments typically work across different countries. Having a grasp of these fundamental processes is necessary when dealing with this data for various purposes. Yet, this foundational knowledge may not always suffice, as awareness of the specific institutional context at the local level is often indispensable. Our humble aim with this post is to offer a starting point for those identifying potential avenues of exploration.

The next post will be about local government autonomy. We will consider some of the formal and pragmatic aspects shaping autonomy, and it’s consequences for policy-making at the local level. We hope you continue to follow our Local Spending Series.

References

Bouley, D., Jacobs, D. F., & Hélis, J. (2009). “Budget Classification,” Technical Notes and Manuals, 2009(006), A001. Retrieved Sep 25, 2023, from https://doi.org/10.5089/9781462343478.005.A001

Fundação Tide Setubal (2019): REGIONALIZAÇÃO DO ORÇAMENTO EM GRANDES CIDADES. Available at: https://fundacaotidesetubal.org.br/midia/publicacao_2988.pdf

Goode, R., & Birnbaum, E. A. (1956). Government Capital Budgets, IMF Staff Papers, 1956(001), A002. Retrieved Sep 26, 2023, from https://doi.org/10.5089/9781451960181.024.A002

Lämmerhirt, D. (2017). “What is the difference between budget, spending, and procurement data?”. Available at: https://blog.okfn.org/2017/05/18/what-is-the-difference-between-budget-spending-and-procurement-data/

Pattanayak, S. (2016). “Expenditure Control: Key Features, Stages, and Actors.” International Monetary Fund. Available at https://www.imf.org/external/pubs/ft/tnm/2016/tnm1602a.pdf

Rankumanr, Vivek, and Shapiro, Isaac. “Guide to Transparency in Government Budget Reports: Why are Budget Reports Important and What Should They Include.” International Budget Partnership. Available at: https://internationalbudget.org/wp-content/uploads/Guide-to-Transparency-in-Government-Budget-Reports-Why-are-Budget-Reports-Important-and-What-Should-They-Include-English.pdf

“The open data handbook”. (2015) Open Knowledge Foundation. Available at:https://opendatahandbook.org/

Wikrent, Katherine. (2017) “A possible tale of tracking ten kilometers of road.” Available at: https://www.open-contracting.org/2017/04/24/possible-tale-tracking-ten-kilometers-road/